Inflation does not destroy lives overnight. It works quietly, almost invisibly, yet with relentless certainty. On the surface, people appear to be living the same daily routines. But underneath, a clear divide is forming—between those who steadily build wealth and those whose lives are slowly being eroded. This gap doesn’t emerge suddenly. It widens day by day, shaped by small, repeated decisions.

Consider an ordinary household. Their income is average. They are not living extravagantly. Yet food prices creep up, utility bills rise, and daily necessities become slightly more expensive. At first, it feels manageable—“just a small increase.” But over months and years, these small increases accumulate. Eventually, savings begin to shrink just to maintain the same lifestyle. Salaries do not rise fast enough to compensate, and the cost of living continues to climb.

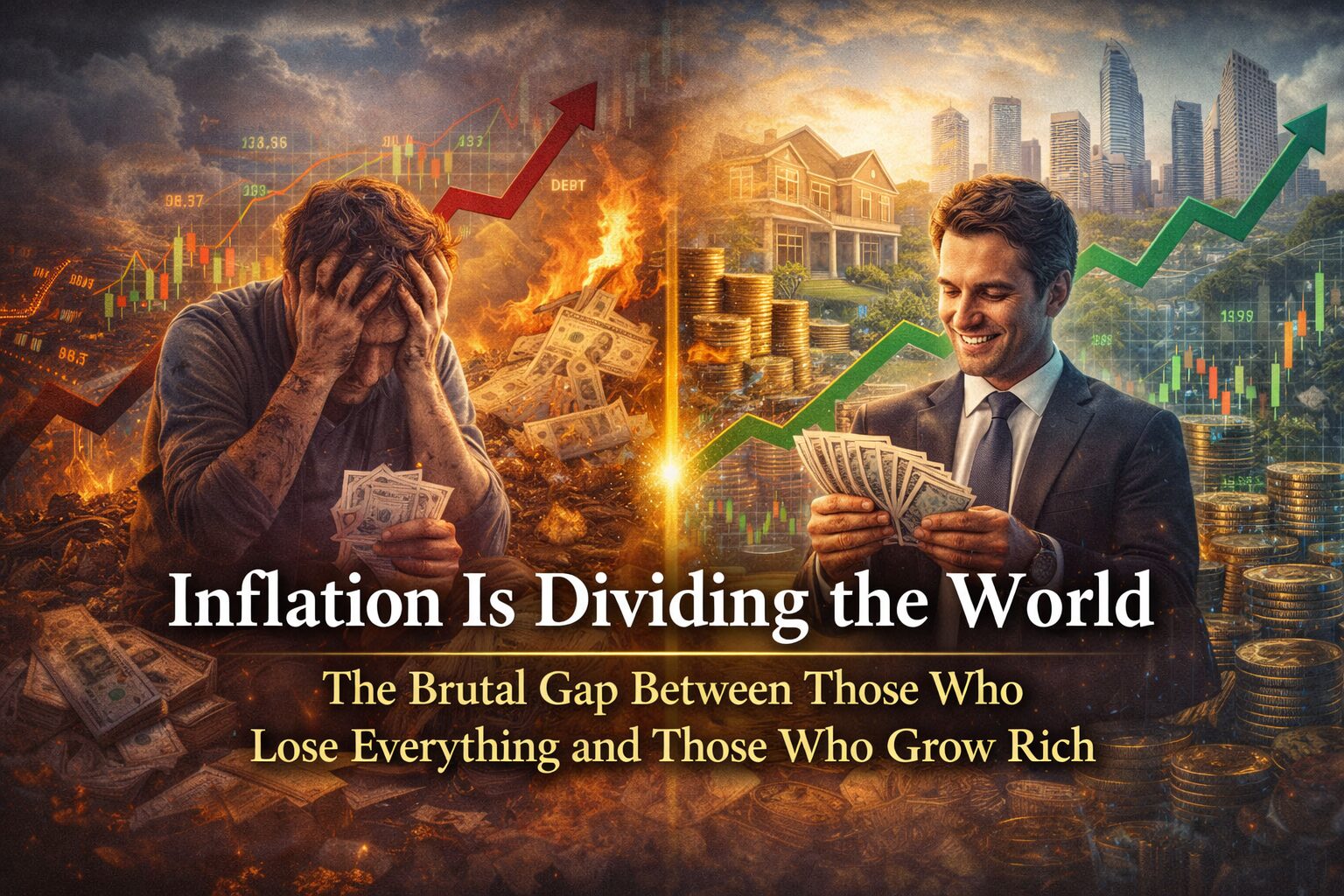

This is where the shift begins. People enter a defensive mode. They cut back on dining out, reduce hobbies, and limit social interactions. Opportunities shrink. Life becomes less about growth and more about survival. This is the quiet poverty that inflation creates—not dramatic, but deeply corrosive.

Now contrast this with another group of people—those who grow wealth during inflation.

They see inflation not as rising costs, but as rising asset prices. Stocks, for example, often increase over time as companies adjust prices and maintain profits. Real estate behaves similarly, maintaining or even increasing its value as currency weakens. While cash loses purchasing power, assets tend to hold or grow their value.

In other words, those who hold only cash are slowly losing, while those who hold assets are positioned to win.

The critical difference lies in information and decision-making speed.

Those who are consumed by inflation tend to choose stability. They keep their money in savings accounts and try to preserve their current lifestyle. But in reality, this is not a neutral choice—it is an active decision to stand on the side where value is guaranteed to decline.

On the other hand, those who build wealth make small but decisive changes. They begin investing. They create additional income streams. They develop skills that increase their earning power. Each step may seem insignificant at first, but over time, these actions compound into a powerful advantage.

The greatest risk in an inflationary era is not taking action.

What feels like “playing it safe” is often the most dangerous path. Even a modest annual inflation rate of 2% significantly reduces purchasing power over a decade. Yet most people remain unaware of this invisible loss. Humans are highly sensitive to visible losses, but surprisingly indifferent to slow, hidden ones.

So how can individuals survive—no, thrive—in an age of inflation?

The answer is simple in theory, but challenging in practice. There are three essential strategies: own assets beyond cash, build multiple income streams, and continuously increase your personal value.

First, assets. Allocate part of your resources into inflation-resistant vehicles such as stocks, mutual funds, real estate, or even gold. Timing the market perfectly is unnecessary. Consistency matters far more. Small, regular investments over time often outperform attempts at perfection.

Second, income streams. Relying solely on a salary is fragile in an inflationary environment. Side businesses, blogging, digital content, freelance work—these do not need to be large. Even a small secondary income creates resilience. The idea you mentioned—publishing English blog content—fits perfectly into this strategy. At first, the income may be small, but over time, it becomes a layer of protection.

Finally, personal value. This may sound abstract, but it is extremely practical. Inflation reduces the value of money—but it increases the relative importance of people who can create value. Skills, knowledge, communication ability, networks—these do not depreciate with inflation. In fact, they become more powerful.

The difference between those who fall into hardship and those who rise is not talent or luck. It is how they respond to change.

Inflation itself cannot be controlled. But your response to it is entirely within your control.

To put it bluntly, in the years ahead, those who drift through life unconsciously will struggle more and more. Meanwhile, those who think slightly ahead and take consistent action will steadily gain an advantage. Massive success is not required. But awareness and action are.

This divide is already happening—right now.

Surviving inflation is not just about protecting money. It is about understanding the system and continuously adjusting your position within it. Only through this ongoing effort can you protect yourself and your family in a world where the gap between winners and losers is quietly, but inevitably, expanding.

コメント